Highlights

World marketed energy consumption is projected to increase by 57 percent

from 2004 to 2030. Total energy demand in the non-OECD countries increases

by 95 percent, compared with an increase of 24 percent in the OECD countries. |

In the IEO2007 reference case—which reflects a scenario where current laws

and policies remain unchanged throughout the projection period—world marketed

energy consumption is projected to grow by 57 percent over the 2004 to

2030 period. Total world energy use rises from 447 quadrillion British

thermal units (Btu) in 2004 to 559 quadrillion Btu in 2015 and then to

702 quadrillion Btu in 2030 (Figure 1). Global energy demand grows despite

the relatively high world oil and natural gas prices that are projected

to persist into the mid-term outlook.

The most rapid growth in energy demand from 2004 to 2030 is projected for

nations outside the Organization for Economic Cooperation and Development

(non-OECD nations). Total non-OECD energy demand increases by 95 percent

in the IEO2007 reference case projection, as compared with an increase

of 24 percent in OECD energy use. The robust growth in demand among the

non-OECD nations is largely the result of strong projected economic growth.

In all the non-OECD regions combined, economic activity—as measured by

GDP in purchasing power parity terms—increases by 5.3 percent per year

on average, as compared with an average of 2.5 percent per year for the

OECD economies.

Trends in end-use sector energy consumption can vary widely, according

to the level and pace of economic development in a given region. In the

OECD region, where energy markets generally are well established, demand

for delivered energy in each of the end-use sectors grows more slowly than

in the non-OECD nations (Figure 2). For the industrial sector, energy-intensive

industries continue to expand more rapidly in the non-OECD countries, where

investors are attracted by lower costs and fewer environmental constraints,

than in the OECD countries. In 1980, the OECD accounted for 52 percent

of the world’s industrial sector energy use. In 2004 the OECD share had

fallen to 44 percent, and it is projected to decline to 33 percent in 2030,

as non-OECD industrial energy use outpaces that in the OECD (Figure 3).

For the OECD countries, industrial sector energy use is projected to grow

at an average rate of 0.6 percent per year from 2004 to 2030; for the non-OECD

countries, the projected increase averages 2.5 percent per year.

As in the industrial sector, energy use in the buildings and transportation

sectors is projected to grow more slowly in the OECD countries than in

the non-OECD countries in the IEO2007 reference case. With slow or declining

population growth in many OECD nations, generally slow growth in energy

use in the buildings sectors is projected, averaging 0.6 percent per year

in the residential sector and 1.1 percent per year in the commercial sector

from 2004 to 2030. For the non-OECD region as a whole, strong growth in

demand for energy is projected in the buildings sectors, averaging 2.4

percent per year in the residential sector and 3.7 percent per year in

the commercial sector.

Historically, growth in transportation activity has been linked closely

to income growth, indicating a strong relationship between per-capita GDP

and passenger car travel per capita, especially in countries with developing

economies. With robust economic growth projected for the developing non-OECD

nations, transportation sector energy use increases by an average of 2.9

percent per year from 2004 to 2030, requiring extensive investment in the

construction of transportation infrastructure (highways, fueling stations,

airport facilities, rail systems, etc.) to support the fast-paced growth

in demand. In the OECD countries, where extensive infrastructure is in

place already and GDP is projected to grow much more slowly, demand for

transportation fuels increases by 0.9 percent per year.

The IEO2007 reference case projects increased world consumption of marketed

energy from all sources over the 2004 to 2030 projection period (Figure

4). Fossil fuels (petroleum and other liquid fuels,1 natural gas, and coal)

are expected to continue supplying much of the energy used worldwide. Liquids

supply the largest share of world energy consumption over the projection

period, but their share falls from 38 percent in 2004 to 34 percent in

2030, largely in response to a reference case scenario in which real world

oil prices remain near the current level through 2030. Liquids remain the

dominant energy source, given their importance in the transportation and

industrial end-use sectors; however, their share of the world energy market

in this year’s outlook is lessened in the projection, as other fuels replace

liquids where possible outside those sectors. Fossil fuel prices in the

reference case also support renewed interest in expanding the use of nuclear

power and renewable energy sources to generate electricity.

World use of petroleum and other liquids grows from 83 million barrels

oil equivalent per day in 2004 to 97 million barrels per day in 2015 and

118 million barrels per day in 2030 in the reference case.2 In most regions

of the world, the role of liquid fuels outside the transportation sector

continues to erode. Liquids remain the most important fuels for transportation,

because there are few alternatives that can compete widely with petroleum-based

liquid fuels. On a global basis, the transportation sector accounts for

68 percent of the total projected increase in liquids use from 2004 to

2030, followed by the industrial sector, which accounts for another 27

percent of the increase.

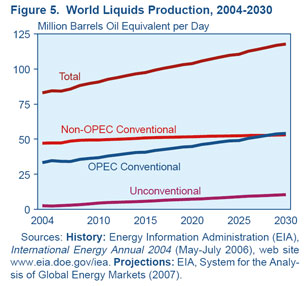

To meet the increment in world liquids demand in the reference case, total

supply in 2030 is projected to be 35 million barrels per day higher than

the 2004 level of 83 million barrels per day. Conventional liquids production

by members of the Organization of the Petroleum Exporting Countries (OPEC)

contributes about 21 million barrels per day to the total increase, and

conventional liquids production in non-OPEC countries adds another 6 million

barrels per day (Figure 5). Unconventional resources (including biofuels,

coal-to-liquids, and gas-to-liquids) from both OPEC and non-OPEC sources

are expected to become increasingly competitive. World production of unconventional

resources, which totaled only 2.6 million barrels per day in 2004, is projected

to increase to 10.5 million barrels per day and account for 9 percent of

total world liquids supply in 2030, on an oil equivalent basis, in the

IEO2007 reference case.

Natural gas consumption increases on average by 1.9 percent per year in

the reference case, from a world total of 99.6 trillion cubic feet in 2004

to 129.0 trillion cubic feet in 2015 and 163.2 trillion cubic feet in 2030.

Rising world oil prices after 2015 increase the demand for—and then the

price of—natural gas, as it is used to displace the use of liquids in the

industrial and electric power sectors. Although natural gas prices vary

by region, they tend to rise as demand increases. Higher natural gas prices,

in turn, make coal more cost-competitive, especially in the electric power

sector. Among the end-use sectors, the industrial sector remains the largest

consumer of natural gas worldwide, accounting for 43 percent of the world’s

total projected natural gas consumption in 2030.

Coal is the fastest-growing energy source worldwide in the IEO2007 reference

case projections. World coal consumption is projected to increase from

114.5 quadrillion Btu in 2004 to 199.1 quadrillion Btu in 2030, at an average

annual rate of 2.2 percent. World coal consumption increased sharply from

2003 to 2004, largely because of a 17-percent increase on a Btu basis in

non-OECD Asia (mainly, China and India). Coal’s share of total world energy

use is projected to increase from 26 percent in 2004 to 28 percent in 2030.

The electric power sector accounts for about two-thirds of the world’s

coal consumption throughout the projection period, and the industrial sector

accounts for most of the remainder. China’s industrial sector is projected

to account for about 78 percent of the total net increase in industrial

coal use worldwide. China has abundant coal resources, limited reserves

of oil and natural gas, and a leading position in world steel production.

World net electricity generation grows by 85 percent in the IEO2007 reference

case, from 16,424 billion kilowatthours in 2004 to 22,289 billion kilowatthours

in 2015 and 30,364 billion kilowatthours in 2030. Most of the projected

increase in electricity demand is in the non-OECD nations, where electricity

generation increases on average by 3.5 percent per year from 2004 to 2030,

as compared with 1.3 percent per year in the OECD nations. Coal and natural

gas remain the most important fuels for electricity generation throughout

the projection period, together accounting for 80 percent of the total

increment in world electric power generation from 2004 to 2030 in the reference

case (Figure 6).

Electricity generation from nuclear power is projected to increase from

2,619 billion kilowatthours in 2004 to 3,619 billion kilowatthours in 2030.

Higher fossil fuel prices, energy security concerns, improved reactor designs,

and environmental considerations are expected to improve the prospects

for new nuclear power capacity in many parts of the world, and a number

of countries are expected to build new nuclear power plants. In the IEO2007

reference case, the world’s installed nuclear capacity grows from 368 gigawatts

in 2004 to 481 gigawatts in 2030. Declines in nuclear capacity are projected

only in OECD Europe, where several countries (including Germany and Belgium)

have either plans or mandates to phase out nuclear power, and where some

older reactors are expected to be retired and not replaced.

Nuclear power generation in the non-OECD countries is projected to increase

by 4.0 percent per year from 2004 to 2030. The largest increase in installed

nuclear generating capacity is expected in non-OECD Asia, where annual

increases in nuclear capacity average 6.3 percent and account for 68 percent

of the total projected increase in nuclear power capacity for the non-OECD

region as a whole. Of the 58 gigawatts of additional installed nuclear

generating capacity projected for non-OECD Asia between 2004 and 2030,

36 gigawatts is projected for China and 17 gigawatts for India. Russia

also is expected to add substantial nuclear generating capacity over the

mid-term projection, increasing capacity by 20 gigawatts.

The use of hydroelectricity and other grid-connected renewable energy sources

is expected to continue to expand over the projection period, increasing

by 1.9 percent per year, at the same rate of growth as natural gas consumption

in the reference case. Higher fossil fuel prices, particularly for natural

gas in the electric power sector, allow renewable energy sources to compete

economically in some areas. Where they are not economically competitive

with fossil fuels, renewable energy sources may be supported by government

policies and incentives. The renewables share of total world energy consumption

is expected to rise from 7 percent in 2004 to 8 percent in 2030.

Much of the growth in renewable energy consumption is projected to come

from mid- to large-scale hydroelectric facilities in non-OECD Asia and

Central and South America, where several countries have hydropower facilities

either planned or under construction. Outside of Canada and Turkey, hydropower

capacity is not expected to grow substantially in the OECD nations, because

most hydroelectric resources in the region already have been developed

or lie far from population centers. Instead, most of the increase in OECD

renewable energy consumption is expected to be in the form of nonhydroelectric

resources, such as wind, solar, geothermal, municipal solid waste, and

biomass.

In recent years, atmospheric concentrations of carbon dioxide—one of the

most important greenhouse gases in the atmosphere—have been increasing

at a rate of about 0.5 percent annually. Because anthropogenic (human-caused)

emissions of carbon dioxide result primarily from the combustion of fossil

fuels for energy, energy use has emerged at the center of the climate change

debate. World carbon dioxide emissions continue to increase steadily in

the IEO2007 reference case, from 26.9 billion metric tons in 2004 to 33.9

billion metric tons in 2015 and 42.9 billion metric tons in 2030, an increase

of 59 percent over the projection period.

From 2003 to 2004, carbon dioxide emissions from the non-OECD countries

grew by almost 10 percent, largely because of a 17-percent increase in

coal use in non-OECD Asia, while emissions from the OECD countries grew

by less than 2 percent. The result of the large increase in non-OECD emissions

was that 2004 marked the first time in history that energy-related carbon

dioxide emissions from the non-OECD countries exceeded those from the OECD

countries—although by only about 8 million metric tons (Figure 7). Further,

because the projected average annual increase in emissions from 2004 to

2030 in the non-OECD countries (2.6 percent) is more than three times the

increase projected for the OECD countries (0.8 percent), carbon dioxide

emissions from the non-OECD countries in 2030, at 26.2 billion metric tons,

are projected to exceed those from the OECD countries by 57 percent.

Notes and Sources |