Based on our research, the national average cost of car insurance is $72 per month for minimum coverage and $223 per month for full coverage

Updated:

Jun 28, 2024

Written by:

Daniel Robinson

Daniel Robinson

Edited by:

Jessica Wackler

Jessica Wackler

Reviewed by:

Mark Friedlander

Mark Friedlander

Insurance Information Institute

Key Takeaways:

- The average cost of car insurance in the U.S. is typically around $869 to $2,681 per year for minimum or full coverage.

- The most affordable car insurance for you will vary based on your unique driver profile, but you can compare averages for drivers with a similar background for a better idea of what you’ll pay.

- Those considered high risk due to a speeding ticket, DUI/DWI, accident or bad credit pay between $299 to $446 on average per month for full coverage.

- Where you live can cause car insurance rates to vary widely, costing as little as $23 per month and as high as $304 per month depending on coverage level and driver profile.

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With our comparison partner,

In this article, we at the MarketWatch Guides team will explain average car insurance costs, the factors that affect car insurance rates and how you can find low prices. As we break down the average cost of car insurance across different states and driver profiles, we’ll also highlight the best car insurance companies to help you find the right match for your budget and coverage needs.

Learn more about our methodology and editorial guidelines.

How Much Does Car Insurance Cost?

Nationally, full-coverage car insurance costs an average of $223 per month or $2,681 per year. For minimum coverage, drivers pay an average rate of $72 per month or $869 per year.

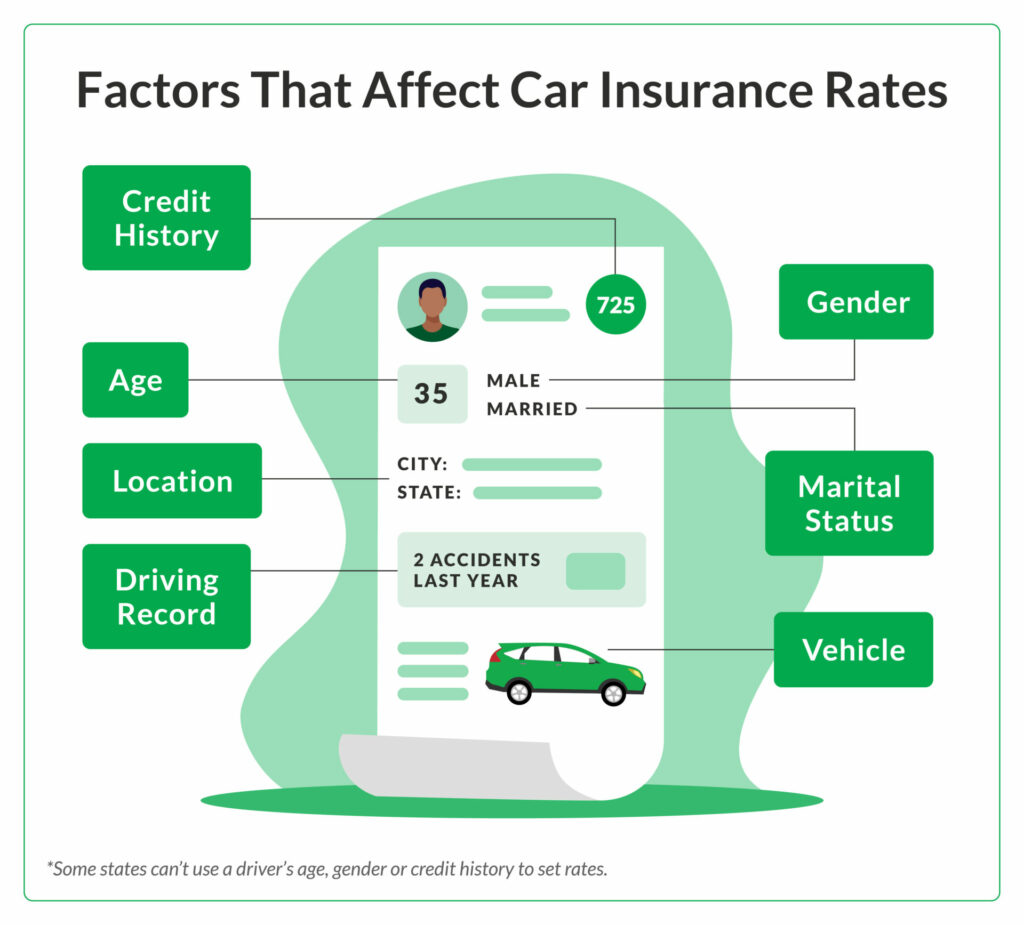

Unless otherwise stated, our rate estimates are based on the profile of a 35-year-old with good credit and a clean driving record — we excluded factors that raise rates. What you might pay for auto insurance coverage depends on multiple factors, including:

Car Insurance Cost by State

State-level driving statistics influence the prices you receive from insurers, and the more densely populated your area is, the higher prices typically are. State laws for minimum-liability car insurance also require different coverage levels, which can affect pricing.

Compare average full-coverage auto insurance rates by state below.

See a full list of minimum- and full-coverage rate estimates by state below, or use the filter feature to view average rate estimates for your home state:

Filters

Location

*All rates featured are average estimates from Quadrant Information Services.

MARKETWATCH GUIDES TIP

Regardless of which state you live in, your rate may be higher if you live in or near a major metropolitan area. In all cases, the best way to see how much car insurance would cost for your vehicle is by comparing free quotes from providers in your area.

Read more: Car Insurance Cost by State

Most Expensive Car Insurance by State

Based on thousands of insurance quotes we received from Quadrant Information Services, Louisiana, New York and Michigan are three of the most expensive states for full-coverage car insurance, followed closely by Pennsylvania and Nevada. We cover some of the reasons behind these sky-high rates below.

| State | Monthly Full-Coverage Rate | Annual Full-Coverage Rate | Difference From National Average 2681 |

| Louisiana | $363 | $4,357 | +63% |

| New York | $343 | $4,112 | +53% |

| Michigan | $339 | $4,067 | +52% |

| Pennsylvania | $326 | $3,909 | +46% |

| Nevada | $322 | $3,870 | +44% |

Why Is Car Insurance So Expensive in These States?

These states are significantly more expensive than the national average, but you may be asking: Why is that the case? New York, Michigan and Pennsylvania are considered no-fault states. In no-fault states, the burden of claim payouts falls automatically on each driver’s insurance company. So even if another driver hits you, your insurance company is the one that pays the bill. To help cover the costs, insurance companies in these states often charge higher premiums.

However, the no-fault system isn’t entirely responsible for high rates. For example, New York also has high rates of insurance fraud. Louisiana and Nevada are actually at-fault states, but have higher highway densities, rates of vehicle theft and rates of crash-related lawsuits.

Read more: Car Theft Statistics 2024

States With the Cheapest Car Insurance

Below, you’ll notice that Maine, Vermont and Hawaii take the top three spots as the most affordable states for full-coverage car insurance. Each state offers rates well below the national average.

| State | Monthly Full-Coverage Rate | Annual Full-Coverage Rate | Difference From National Average |

| Maine | $122 | $1,460 | -46% |

| Vermont | $128 | $1,539 | -43% |

| Hawaii | $132 | $1,581 | -41% |

| Idaho | $132 | $1,588 | -41% |

| Ohio | $138 | $1,660 | -38% |

Why Is Car Insurance Cheaper in These States?

Of the five states listed above, only Hawaii is a no-fault state. Often, no-fault states have higher insurance rates. However, Hawaiian law prevents insurance companies from using a driver’s age, gender or credit history to determine rates. These restrictions stabilize the cost of insurance and drive rates lower for most drivers.

States like Maine have low population density and lower rates of uninsured drivers than other states, meaning insurers face fewer financial risks when writing premiums. As a result, companies are able to offer lower premiums in these locations.

Estimate Car Insurance Cost

Find the average costs of car insurance in your state for full coverage using our free car insurance calculator below.

Note: The calculators used on this website should be used for educational purposes only. Data will not be collected or stored. The results are estimates based on the information provided and may not reflect the actual pricing of your quote.

Car Insurance Cost by Provider

Because providers weigh risk factors differently, your rate will also vary depending on the provider you choose. For most major providers, however, you can still expect rates below the national average of $223 per month or $2,681 per year.

Among well-known large and midsize insurers in the U.S., USAA offers the lowest full-coverage insurance rates on average at just $145 per month. However, this coverage is only available for military members and their families. For most other drivers, Erie Insurance is an affordable choice at $158 per month for a similar comprehensive policy.

| Car Insurance Company | Monthly Full-Coverage Rate | Annual Full-Coverage Rate |

| USAA | $145 | $1,741 |

| Erie Insurance | $158 | $1,894 |

| Geico | $166 | $1,995 |

| Nationwide | $172 | $2,063 |

| Progressive | $194 | $2,326 |

| State Farm | $212 | $2,544 |

Read more: Best Car Insurance Companies or Cheapest Car Insurance Companies

Car Insurance Cost by Age

Younger drivers with their own insurance policies tend to pay the most for car insurance due to a lack of driving experience, which translates to higher insurance rates. Seniors older than 75 also pay slightly higher rates overall than those between 25 and 55 years old, because they’re more likely to get into car accidents due to weaker vision and motor skills.

Here’s a look at average full-coverage auto insurance costs for various age groups:

| Age | Monthly Full-Coverage Rate | Annual Full-Coverage Rate |

| 16 | $519 | $6,226 |

| 17 | $499 | $5,989 |

| 18 | $472 | $5,669 |

| 19 | $433 | $5,192 |

| 21 | $349 | $4,186 |

| 25 | $256 | $3,070 |

| 35 | $223 | $2,681 |

| 45 | $214 | $2,565 |

| 55 | $198 | $2,375 |

| 65 | $202 | $2,425 |

| 75 | $232 | $2,788 |

MARKETWATCH GUIDES TIP

Young and older drivers tend to pay the most for car insurance, but that doesn’t mean there aren’t plenty of savings opportunities and good car insurance companies that work better for certain ages.

Read more: Best Car Insurance for Young Drivers, Senior Drivers or New Drivers

Car Insurance Cost for High-Risk Drivers

Auto insurers have to weigh the risk factors in every driver’s record. If you have one or more speeding tickets, at-fault accidents or other violations in your driving history, you’ll pay higher premiums than those with clean records. Having bad credit also heightens the risk for insurance providers and can be used to determine rates in most states.

Here’s a look at how average full-coverage rates change for 35-year-olds after different driving violations:

| Driving Record | Monthly Full-Coverage Rate | Annual Full-Coverage Rate | Rate Difference From Low-Risk Drivers |

| Clean | $223 | $2,681 | N/A |

| Speeding ticket | $270 | $3,235 | 21% |

| DUI | $323 | $3,874 | 44% |

| At-fault accident | $299 | $3,591 | 34% |

| Bad credit | $446 | $5,358 | 100% |

MARKETWATCH GUIDES TIP

If you work with your insurance provider and practice good driving habits, you may be able to lower your insurance rates over time. Speak with your insurance agent about discounts for taking defensive driving courses or ask about accident forgiveness policies. If you’re looking for a new provider, consider several options. In many cases, Progressive or State Farm can be affordable choices for high-risk drivers.

Read more: Best High-Risk Car Insurance

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With our comparison partner,

Car Insurance Cost by Vehicle Type

The type of vehicle you drive plays a role in setting your car insurance rates. The good news is that drivers of most vehicle types often pay rates below the national average of $223 per month or $2,681 per year. However, EV drivers can pay as much as 31% more.

Below, we’ll show how full-coverage insurance averages change based on vehicle type.

| Vehicle Type | Average Monthly Rate | Average Annual Rate |

| Sedans | $220 | $2,635 |

| Trucks | $203 | $2,439 |

| SUVs | $195 | $2,339 |

| Hybrids | $196 | $2,357 |

| Electric Vehicles (EVs) | $293 | $3,520 |

We go into why prices vary so much between vehicle types below:

- Standard sedans: Standard sedans are often the cheapest to insure due to low passenger capacity and low replacement costs.

- Trucks: While they can be more expensive to repair and replace, their low passenger capacity makes them more affordable than SUVs and higher-end cars.

- SUVs: Because of their larger size and capacity for more passengers, these vehicles often cause more damage and injuries during accidents.

- Hybrid and electric vehicles: Parts and labor for these vehicles can be pricey, which means you’ll pay higher premiums for full-coverage policies for hybrids and EVs.

- Sports cars: Vehicles built for speed and performance are at higher risk of causing accidents. Sports cars also tend to have higher costs for replacement parts.

- Luxury cars: As with sports cars, replacement parts for luxury vehicles are more expensive than for standard daily drivers. The high purchase price also leads to greater insurance premiums.

Car Insurance Cost by Model

While the type of vehicle you drive can impact your insurance rates, so can the make and model. Each vehicle has different reliability ratings, replacement and repair costs, safety features and driving statistics that affect your rates. If your car costs more to repair, it’ll likely also cost more to insure.

Read more: Cheapest Cars To Insure or Most Expensive Cars To Insure

We received quotes from well-known insurance providers for several popular vehicle makes and models. In general, most models are affordable compared to the national full-coverage average of $2,681 per year or $223 per month. However, select electric vehicles from companies like Kia and Tesla stand out as more expensive than the rest. In most cases, electric vehicles cost more to insure because they cost more to repair.

| Vehicle Model | Monthly Full-Coverage Rate | Annual Full-Coverage Rate |

| Chevy Equinox | $188 | $2,253 |

| Chevy Malibu | $217 | $2,602 |

| Chevy Silverado | $205 | $2,458 |

| Ford Bronco | $183 | $2,192 |

| Ford Escape Hybrid | $189 | $2,266 |

| Ford F150 | $203 | $2,438 |

| GMC Acadia | $212 | $2,546 |

| GMC Sierra | $202 | $2,418 |

| Honda CRV Hybrid | $185 | $2,223 |

| Honda Civic | $209 | $2,507 |

| Honda Ridgeline | $205 | $2,455 |

| Hyundai Elantra | $223 | $2,681 |

| Hyundai Ioniq | $226 | $2,709 |

| Hyundai Santa Fe | $207 | $2,486 |

| Kia Forte | $233 | $2,799 |

| Kia Sportage | $192 | $2,298 |

| Nissan Altima | $248 | $2,981 |

| Nissan Frontier | $200 | $2,396 |

| Nissan Leaf | $210 | $2,519 |

| Nissan Rogue | $210 | $2,517 |

| Subaru Crosstrek | $185 | $2,214 |

| Subaru Impreza | $186 | $2,233 |

| Tesla Model 3 | $305 | $3,664 |

| Tesla Model S | $399 | $4,786 |

| Tesla Model X | $376 | $4,516 |

| Tesla Model Y | $286 | $3,426 |

| Toyota Prius | $215 | $2,582 |

| Toyota Rav4 | $194 | $2,325 |

| Toyota Tacoma | $205 | $2,460 |

| GMC Hummer EV | $352 | $4,221 |

| Kia EV6 | $256 | $3,067 |

| Chevy Silverado EV | $228 | $2,740 |

Car Insurance Cost by ZIP Code

A variety of ZIP code-specific information such as crime, weather, driving statistics and population density are used to determine car insurance costs. Typically, the more urban your area is, the more expensive your car insurance is. Some states may have ZIP codes with rate differences of over 100%.

Below, you can read more about how your ZIP code can affect your rates and compare car insurance in your area.

Read more: Where Does ZIP Code Matter Most for Car Insurance Rates?

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With our comparison partner,

Other Car Insurance Cost Factors To Know

In the section below, we detail the most common factors that affect your car insurance rates:

| Car Insurance Rate Factor | Factor Description |

| Mileage | If you drive fewer miles per year than most drivers, you’re less of a risk to insure and may receive lower premiums. |

| Home ownership | Homeowners often get discounted insurance rates for bundling policies, meaning rates are sometimes lower for these drivers. |

| Marital status | In many states, married drivers pay less than single drivers on average. |

| Occupation | Some professionals like teachers and government employees may get occupation or affiliation discounts. |

| Market conditions | Insurance costs fluctuate with the market. If other costs have inflated, your insurance rates may have, too. |

| Vehicle manufacturer issues | If your vehicle’s car brand has issues with break-ins, safety feature failures and recalls, insurance companies could consider it a higher risk to insure, meaning higher rates. |

| Vehicle ownership status | Leased and financed cars need both comprehensive and collision coverage, making them more expensive to insure. Insurers also view those with liabilities to their car as more risky, increasing the cost of a policy. |

| Number of policy members | The more people and cars you have on your policy, the cheaper the per-person costs typically are. |

| Insurance history | If you’ve had any lapses in coverage or claims, your rates will be higher. The longer you have continuous coverage and the fewer claims you have, the less risk you’ll represent to insurance companies. |

Are You Paying Too Much for Car Insurance?

If you’ve had a policy for over six months, you may be paying too much for car insurance. The best way to check whether you’re overpaying for car insurance is to compare your rate against the average for your coverage level in your state and your driver profile. Comparing multiple company quotes with the same coverage you have will allow you to gauge whether you’re getting a good deal.

How To Get Lower Car Insurance Costs

If you’re shopping for car insurance online and are receiving quotes that are outside your budget, here are several strategies to save money:

Shop around: It’s worth comparing rates from several insurers before you commit to a contract. Since insurance companies weigh risk factors differently, you may qualify for a lower car insurance premium from another provider.

Read more: How To Shop for Car Insurance

Bundle plans: Bundling your home and auto insurance policies typically results in premium discounts. You can also save money by insuring multiple vehicles under the same car insurance policy.

Pay up front: Most insurers offer a pay-in-full discount. If you’re able to pay your entire premium at once, it’s often a more cost-effective option.

Take a class: Every state offers state-approved driver safety programs. Depending on the state, these classes are around six or eight hours long. Most insurers offer discounts for the completion of these programs.

Use a monitoring app: Several providers offer usage-based discounts or usage-based insurance programs. After signing up, you’ll monitor your driving habits through an app that tracks things like braking distance, average speed and driving times and rewards you for good behavior on the road.

Reduce coverage: As your vehicle ages, you may no longer need comprehensive and collision insurance policies. The rule of thumb is that you should drop coverage when your annual premium exceeds 10% of your vehicle’s total value.

Utilize discounts: Car insurance companies offer discount opportunities to help customers save on their premiums. We’ll cover a larger breakdown of discount offerings from car insurance providers in the section below.

Compare quotes before renewal: Out of 2,000 drivers we surveyed, only 11% of respondents said they shopped for auto coverage every six months, while just over half reported doing so less than once a year. While sticking with your current insurer feels natural, factors that impact your rates may have changed. You could save on premiums by comparing rates from other providers before you renew.

Read more: How To Switch Car Insurance

Read more: How To Save Money on Car Insurance

Recommended Discounts by Driver Profile

See below to find the discounts we recommend for drivers like you.

Adult drivers with a history of safe driving and good credit already pay the lowest car insurance rates in the industry. However, if you fit this description you may still be able to save on your premiums using one or more of the following discounts:

- Paperless billing: Many insurance companies, including State Farm and Progressive, offer small rate discounts for enrolling in paperless or online billing.

- Good driver discounts: If you’ve changed insurance companies in the last year and maintained good driving habits, be sure to check in about good driver discounts at policy renewal time.

- Pay-in-full discount: If you pay your six-month or annual policy premium in full upfront, companies like State Farm may offer you a discounted rate.

- New vehicle discount: Well-known insurance companies like Geico and State Farm offer discounted coverage rates for new vehicles.

Drivers between the ages of 16 and 19 pay the highest car insurance rates on average. Still, parents and teens can take advantage of the following discounts to save on premiums:

- Driver’s education discount: Teen drivers enrolled in an approved driver’s ed course can receive special discounts from providers like Geico or State Farm.

- Distant student discount: Sometimes referred to as a “student away at school” discount, this special rate reduction from providers like Progressive or Travelers helps college students maintain insurance coverage even while away from their vehicles.

- Good student discount: Students who maintain good grades and attendance can get up to 25% off of their insurance premiums from providers like State Farm.

- Vehicle safety features: Teen drivers can save on car insurance premiums if their vehicles have qualifying safety restraints, airbags and other features, giving parents both peace of mind and a budget break.

Middle-aged and senior drivers enjoy lower rates and have access to a wider range of discount opportunities than many drivers. If you’re looking for ways to save on your car insurance premiums, consider the discounts below:

- Homeowner’s discount: Companies like Progressive offer discounts for drivers who own a home.

- Multiple policy discount: If you have any combination of renter’s, homeowner’s, life and car insurance policies with providers like Travelers or Geico, you may qualify for a multi-policy discount.

- Loyalty discounts: Insurers like State Farm often offer discounts for renewing your policy with the company or for staying with the company for a number of years.

- Senior discount: Geico is one of the few companies that offers special discounts for drivers over 55. The company also offers a guaranteed renewal program that means you won’t be denied coverage based on your age.

If you’ve recently been in an accident or received a speeding ticket, you may be on the hunt for lower insurance rates. We recommend insurance agent whether you qualify for any of the following types of discounts:

- Accident forgiveness: Progressive and State Farm each offer add-on accident forgiveness coverage, which typically forgives one accident per policy period, for well-qualified drivers.

- Defensive driving: If you have a recent speeding ticket or other traffic violations, you may be able to take an approved defensive driving course to lower your insurance rates with companies like Progressive or Geico.

- Driver training: Similar to defensive driving courses, driver re-education courses help you establish better habits on the road and may qualify you for select insurance discounts.

- Low-mileage discount: If you don’t drive your main vehicle frequently, either while on base or deployed, you could qualify for lower car insurance rates.

- Military discount: Beyond USAA, providers like Geico offer discounts for retired and active-duty military members.

- Vehicle storage discount: If you plan on storing your vehicle while deployed, discuss the possibility of a vehicle storage discount with your insurance agent.

Read more: Car Insurance Discounts Guide

Why Did My Car Insurance Rates Go Up?

Aside from changes in personal factors, there have been continuing high levels of inflation, increasing prices for car insurance and the general market. According to the Bureau of Labor Statistics, since 2022, the consumer price index for auto insurance has drastically increased by 40.5%. Factors such as the COVID-19 pandemic and the rising prices of cars, parts and repair services have caused most of this rise in insurance rates.

Read more: Is Car Insurance Getting Worse in 2024? or What To Do About Rising Insurance Rates

Average Car Insurance Price: The Bottom Line

After conducting in-depth industry research, our team found that the average full-coverage policy costs $2,681 per year or $223 per month on average. This is higher than minimum liability coverage because it incorporates liability, comprehensive and collision insurance. Minimum liability coverage costs $869 per year or $72 per month on average.

You should expect your rate to differ from national averages for a variety of reasons. To find the best car insurance price, we recommend shopping around and comparing car insurance rates from reputable insurance providers.

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With our comparison partner,

Best Value Car Insurance Providers

The cost of car insurance is an important thing to consider when choosing a provider. Of course, you’ll also want to pick a reputable insurer that offers good coverage and has a simple claims process. Here are a few providers we recommend.

State Farm: Best Customer Experience

Affordable rates, a variety of coverage options and excellent customer service combine to make State Farm our choice for Best Customer Experience. Full-coverage rates from State Farm average out at $2,544 per year or $212 per month, around 5% less than the national average. State Farm also scored high across multiple areas of the J.D. Power 2023 U.S. Auto Insurance Study℠, which polled customer satisfaction in different regions.

The company offers all the standard insurance products you’d expect (liability, collision, comprehensive, underinsured/uninsured motorist coverage, personal injury protection (PIP) and medical payments (MedPay), along with the following optional types of protection:

- Roadside assistance

- Rental car reimbursement

- Rideshare insurance

- Travel expense* coverage

- Accident forgiveness coverage

*Up to $500 for food and lodging when you break down 50 miles or more from home

In our experience with State Farm, claims can take a while. However, access to friendly local agents made navigating claims easier overall.

Learn more about the provider in our complete State Farm insurance review.

Geico: Best for Budget-Conscious Drivers

Geico offers low premiums across the country, evident in the company’s national rate average of $1,995 per year or $166 per month. That’s about 26% less than the national average. When conducting our insurance cost research, we often found Geico to be the cheapest insurer.

The company also has a good customer service reputation — it has an A+ rating from the Better Business Bureau (BBB). In our experience with Geico, we found that the claims process can take a while and requires working closely with your adjuster. However, the company paid out appropriately for claims and didn’t raise our rates afterward.

Geico offers the six standard types of auto insurance, as well as the following add-on coverage options:

- Emergency roadside service

- Rental car reimbursement

- Mechanical breakdown insurance

- Accident forgiveness coverage

Learn more about the provider in our complete Geico car insurance review, or see our comparison of Geico and State Farm.

Progressive: Best for Tech-Savvy Drivers

According to our research, Progressive is a particularly good option for high-risk drivers such as young drivers, elderly drivers and drivers with a DUI on record. We found that Progressive tends to offer the most competitive rates for these types of drivers, who will often find insurance policies quite expensive. For example, the company’s average rates for a driver with a recent DUI are $2,696 per year or $225 per month, over 30% less than the national average of $3,874 per year for drivers with a similar history.

When our team worked with Progressive, we found that filing a claim with the company was quick and easy, and the payout was quick after we handled our deductible.

Progressive sells all standard insurance policies as well as the following add-on coverages:

- Loan/lease payoff

- Rental car reimbursement

- Custom parts and equipment value coverage

- Rideshare coverage

- Roadside assistance

- Accident forgiveness coverage

We also named it Best for Tech-Savvy Drivers because of its helpful online tools and usage-based insurance options.

Learn more about the provider in our complete Progressive car insurance review or see how Progressive compares to Geico or State Farm.

Average Cost of Car Insurance: FAQ

Below are frequently asked questions about the average car insurance rates:

The average cost of car insurance for full coverage is $2,681 per year or $223 a month. Minimum liability coverage costs an average of $869 per year or $72 per month. However, your costs will vary depending on factors such as age, location, credit score and driving record.

If you have a full-coverage car insurance policy, $100 per month is a very affordable cost. In fact, our research shows that the national average for full coverage is $223 per month. For a minimum-liability policy, the national average is around $72 per month.

State Farm is both the largest auto insurer in the country and the winner of our Best Customer Experience award. According to the National Association of Insurance Commissioners (NAIC), State Farm holds 18.3% of the market share. The company wrote about $58 billion in direct premiums in 2023.

According to our research, full-coverage car insurance for an 18-year-old driver costs $5,669 per year or $472 per month on average if they purchase their own policy. Thankfully, many providers offer discounts for adding a teen driver to your family policy.

It’s generally cheaper to pay your car insurance premium annually. This is because insurers often package processing costs into each installment if you pay monthly or quarterly. Most providers also offer a discount if you pay in full up front.

Michigan has the highest average car insurance costs in the country. According to our research, the average cost of a full-coverage policy in the state is $3,643 per year or $304 per month.

How We Calculate Average Car Insurance Rates

Our comprehensive rating system utilizes the latest 2024 insurance rates from Quadrant Information Services in combination with data we’ve collected on dozens of insurance companies. To help consumers get the most accurate picture of insurance rates nationally, we’ve averaged rates from providers across all 50 states. Unless otherwise specified, our base driver profiles for car insurance quotes include male and female drivers, age 35, driving a 2023 Toyota Camry with a clean driving record and good credit.

We’ve also looked at quotes for drivers of multiple ages and those with a history of accidents, speeding tickets or DUIs, as well as drivers with poor credit. Our minimum-coverage quotes reflect coverage that meets mandatory insurance minimums in each state, while our full-coverage quotes reflect the following coverage amounts:

✓ $50,000 per person in bodily injury coverage

✓ $100,000 per accident in bodily injury coverage

✓ $50,000 per person in property damage coverage

✓ $500 comprehensive coverage deductible

✓ $500 collision coverage deductible

Unless otherwise noted, providers in this piece are presented unranked with accompanying rate averages. However, when rating providers nationally, we take several factors into account:

- Coverage (30% of total score): Companies that offer a variety of choices for insurance coverage are more likely to meet consumer needs.

- Cost and Discounts (25% of total score): Auto insurance rate estimates generated by Quadrant Information Services and discount opportunities are both taken into consideration.

- Industry Standing (20% of total score): Our research team considers market share, ratings from industry experts and years in business when giving this score.

- Customer Experience (15% of total score): This score is based on volume of complaints reported by the National Association of Insurance Commissioners (NAIC) and customer satisfaction ratings reported by J.D. Power. We also consider the responsiveness, friendliness and helpfulness of each insurance company’s customer service team based on our own shopper analysis.

- Availability (10% of total score): Auto insurance companies with greater state availability and few eligibility requirements score highest in this category.

Our credentials:

- 800 hours researched

- 130+ companies reviewed

- 8,500+ consumers surveyed

*Data accurate at time of publication.

If you have feedback or questions about this article, please email the MarketWatch Guides team at editors@marketwatchguides.

Related Resources