You’ll typically be required to purchase new car insurance before you drive your new vehicle off the dealership lot or before the grace period ends.

Discover if you are overpaying for car insurance below.

Partner content: This content was created by a business partner of Dow Jones, independent of the MarketWatch newsroom. Links in this article may result in us earning a commission. Learn More

You’ll typically be required to purchase new car insurance before you drive your new vehicle off the dealership lot or before the grace period ends.

Discover if you are overpaying for car insurance below.

With our comparison partner,

Key Takeaways:

For the most part, getting new car insurance is pretty similar to buying coverage for any other vehicle. There are some particulars, however, and you may have different needs when it comes to insuring a new car than if you were protecting a used one.

We at the MarketWatch Guides Team take an in-depth look at how to get auto insurance for a new car, from the essential types of coverage to how much it might cost you. We also share a few recommended providers from our list of the best car insurance and cheapest car insurance companies to help you get started.

With our comparison partner,

Learn more about our methodology and editorial guidelines.

You should get insurance for a new car as soon as possible since most vehicle dealerships require proof of insurance before you drive off with a new vehicle. However, when you need to get the insurance depends on whether the dealer offers a grace period, which gives you time after purchase to get a car insurance policy. Even with this in mind, we recommend that you compare policies from multiple car insurance providers before purchasing a new car.

If a company offers a grace period, it typically lasts seven to 30 days from the date of purchase. This grace period is a set amount of time in which you’re allowed to drive your vehicle without starting a new insurance policy. Whether you have a grace period depends on a few factors, including:

Since grace periods vary from company to company, it’s best to figure out exactly what your policy will allow for. You can find this information in the fine print of your contract, but it may be easier to ask an insurance agent.

If you buy insurance before taking ownership of a new car, the policy will begin the moment you drive your vehicle off the lot. This is often required by dealerships because it’s illegal for anyone to drive without auto insurance.

You’ll need the following information on hand to start a new car insurance policy before buying the vehicle:

Most car insurance providers will be able to start your policy within 24 hours. You can even find same-day insurance from many auto insurance companies.

According to our research, the national average cost of full-coverage car insurance is $2,681 per year. Your premium, however, is likely to vary based on personal and car-specific factors.

Technically speaking, whether a car is new or used doesn’t factor into your premiums. However, you’ll see rates go up for a new car if it’s more expensive overall than your previous car.

In our research, we found that Travelers tends to be the best overall car insurance provider due to its affordable rates, coverage options and customer service. However, there are several other providers worth considering as well, if you’re looking for the best insurance for your new car.

| Car Insurance Provider | Overall Rating | Annual Cost Estimate |

|---|---|---|

| Travelers | 9.5 | $1,692 |

| Progressive | 9.4 | $2,326 |

| Geico | 9.3 | $1,995 |

| USAA | 9.3 | $1,741 |

| Erie Insurance | 9.2 | $1,894 |

| Nationwide | 9.2 | $2,063 |

| State Farm | 9.2 | $2,544 |

| Liberty Mutual | 9.1 | N/A |

| Allstate | 8.1 | $3,340 |

| American Family Insurance | 9 | $2,700 |

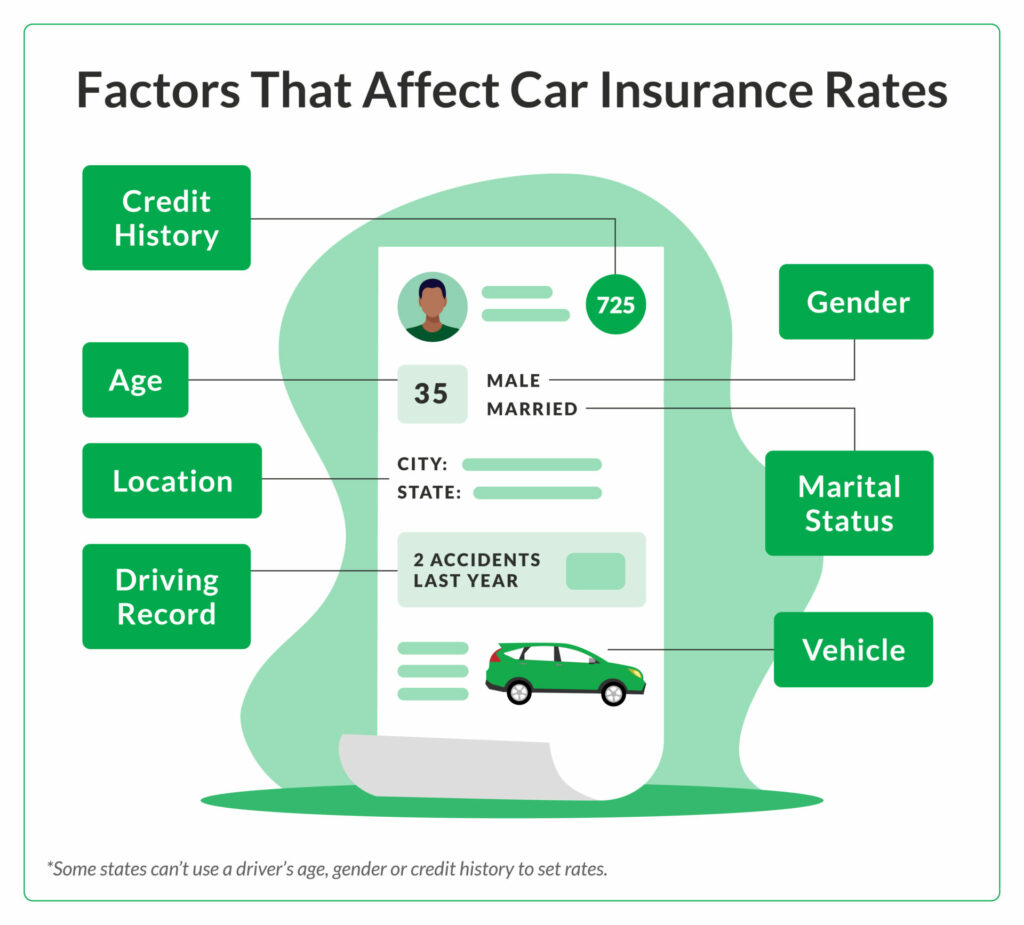

The value of your vehicle is just one of many factors that insurers use to determine premiums. When you insure any vehicle, new or used, several things are taken into account, like your age, driving history and credit score.

Here are additional factors that affect the cost of car insurance:

Buying a new car insurance policy is mostly the same as getting insurance for any other car. With most insurers, you should be able to find coverage, purchase it and start your policy while you wait at the dealership.

The process for getting new car insurance coverage is relatively simple. You’ll just need to follow these steps:

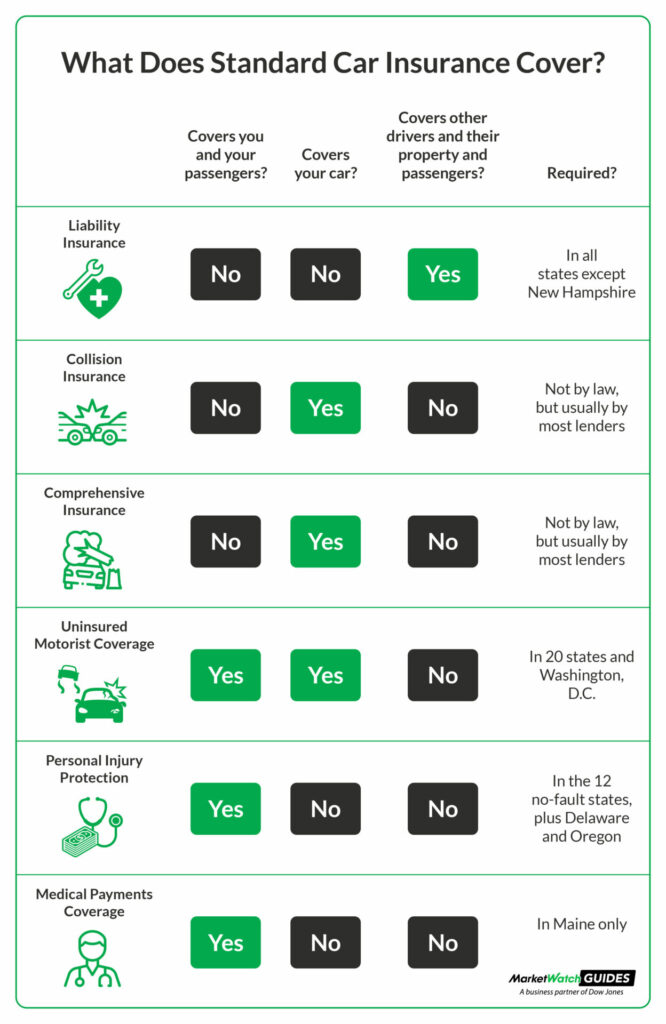

For the most part, new cars don’t require any different types of insurance coverage than other vehicles. The kinds and amounts of coverage you need depend on other factors, such as where you live and whether your lender has extra requirements if you take out a new car loan.

Each state has its own minimum insurance requirements. Usually established by the state’s department of motor vehicles (DMV) or a similar agency, these standards often vary widely.

You can find your state’s requirements and our recommendations for providers with cheap rates by clicking your state on the map below:

State minimum requirements are almost always made up of some variation of the auto insurance coverage options listed below.

Some lenders require borrowers to carry new car insurance add-ons that cover damages to the vehicle in every circumstance. This is meant to protect the lender’s financial interest. That’s why you may be required to carry additional coverage options like these if you take out a loan to buy a new car:

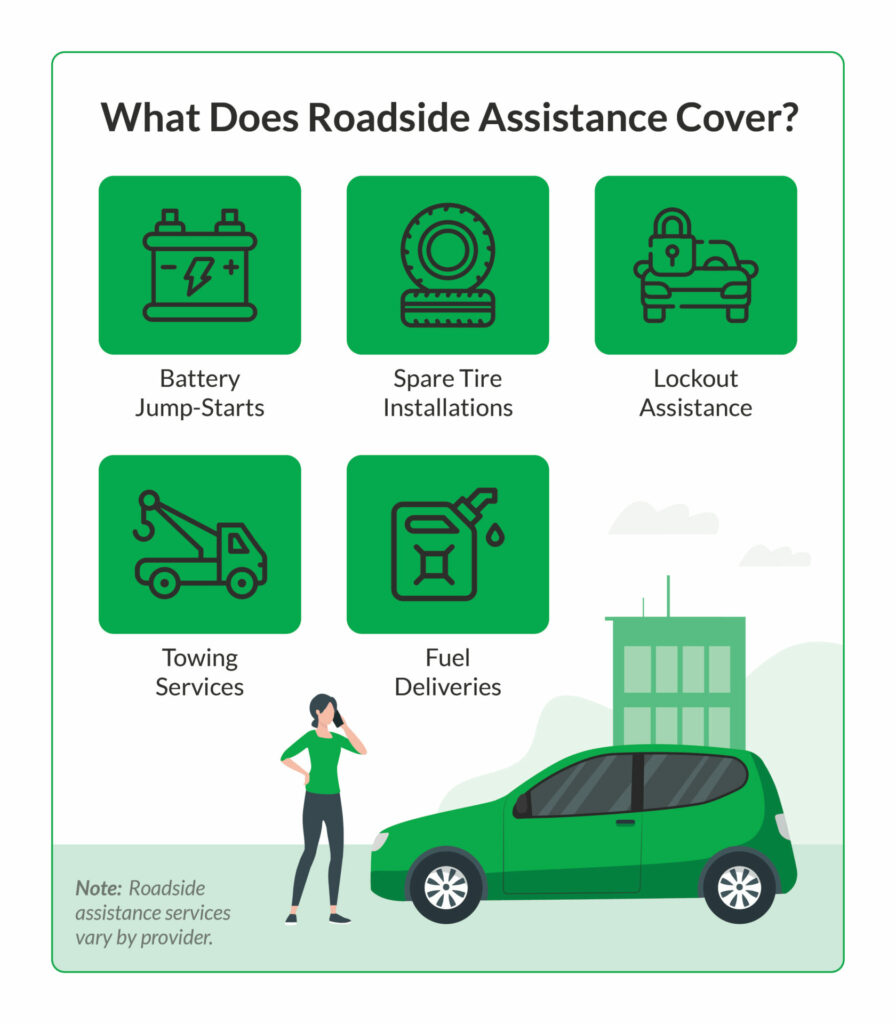

While standard options are mostly the same from one provider to the next, many insurance companies differentiate themselves through additional choices. Many of these add-ons help to manage other aspects of new car ownership, such as breakdowns and emergencies.

Some of the most common optional coverages you’ll find are:

Most auto insurers offer unique lineups of optional new car insurance coverages. You can learn about all available options as well as what each plan covers by speaking with an agent.

It’s best to get auto insurance for a new car before you buy it — and in many cases you’ll be required to. Thankfully, you have the ability to quickly get car insurance quotes online or over the phone with policies that can start the same day, if needed. We recommend that you compare car insurance quotes from multiple insurers before purchasing a new vehicle.

It’s so easy to shop around for car insurance that you can probably do it while you wait for the financing department or another delay that’s involved in buying a car. Our team recommends State Farm and Travelers as good places to start your search.

If you’re looking for affordable coverage and a wide selection of options, you may want to check out Travelers. We found that the company has an ample coverage portfolio, with many of Travelers’ choices appealing to owners of new vehicles. For example, Premier New Car Replacement® will cover the cost of a brand-new replacement of the same make and model in the event of a total loss.

Keep reading: Travelers insurance review

State Farm is the nation’s largest insurer and another solid choice for coverage. Drivers can often find inexpensive new car insurance through State Farm, and the company also offers an extensive selection of additional coverage options. With a large number of insurance discounts to choose from, State Farm policyholders can get the coverage they want at affordable rates.

Keep reading: State Farm insurance review

With our comparison partner,

Below are some frequently asked questions about new car insurance.

Buying auto insurance for a new vehicle works pretty much the same as it does on any car. With new car insurance, you typically have to buy it before you actually own the car. Most dealers and dealerships require proof of insurance to transfer ownership of the vehicle to you.

A new car is usually more expensive to insure than the one it replaces, but that’s not just because you’re the car’s first owner. New vehicles are typically more expensive to insure because they’re worth more and the value of a car is a major factor in the cost of auto insurance.

Legally, you only need to carry your state’s minimum required insurance for a new car. However, if you took out a loan to buy your new vehicle, your lender may require you to carry additional types of insurance.

How long you have to add a new car insurance policy depends on your specific insurer. Some companies offer a grace period, which is usually somewhere between seven and 30 days. However, this mainly applies if you had a policy on your previous vehicle that’s still active. Legally, you’ll need to have car insurance any time you take your new car out on the road.

Before buying a policy for your new car, consider how much coverage you need for yourself and your car — and how much coverage you can actually afford. As you compare companies, look into each provider’s customer service reputation, including its claims service and responsiveness.

In general, it’s best to buy auto insurance before you get a new car. If you already have insurance for another vehicle, you likely won’t need a new plan. Most companies offer a short grace period where your new car is covered. Depending on the dealership, however, you may have to show proof of insurance if you’re planning to buy a new car with a loan.

Overall, we found that Travelers offers solid coverage for new vehicles. The company has the best combination of cheap rates, high customer satisfaction and coverage options for drivers to choose from.

During our research, we found that new car insurance can cost as much as 10% more than for a vehicle with an older make and model. New vehicles tend to cost more to insure because they’re initially worth more money until they begin to depreciate in value. They’re also more likely to get stolen and will cost more to repair.

Because consumers rely on us to provide objective and accurate information, we created a comprehensive rating system to formulate our rankings of the best car insurance companies. We collected data on dozens of auto insurance providers to grade the companies on a wide range of ranking factors. The end result was an overall rating for each provider, with the insurers that scored the most points topping the list.

Here are the factors our ratings take into account:

Our credentials:

*Data accurate at time of publication.

If you have feedback or questions about this article, please email the MarketWatch Guides team at editors@marketwatchguides.