Chapter 3 - Petroleum and Other Liquids Fuels

| World liquids consumption in the IEO2007 reference case increases from 83 million barrels per day in 2004 to 118 million barrels per day in 2030. Two-thirds of the increment is projected for use in the transportation sector. |

In the IEO2007 reference case, world consumption of

petroleum and other liquid fuels4 grows from 83 million

barrels oil equivalent per day in 2004 to 97 million in

2015 and 118 million in 2030. The demand for liquids

increases strongly in the projections, despite world oil

prices that remain above $49 per barrel5 throughout the

period. Much of the overall increase in liquids consumption is projected for the nations of non-OECD Asia,

where strong economic growth is expected.

To meet the increase in liquids consumption in the

IEO2007 reference case, liquids production is projected

to increase by 14 million barrels per day from 2004 to

2015 and by an additional 20 million barrels per day

from 2015 to 2030. OPEC producers6 are expected to provide more than one-half of the additional production in

2015 (8 million barrels per day) and more than two

thirds in 2030 (23 million barrels per day).

In the reference case projections, sustained high world

oil prices support a substantial increase in non-OPEC

liquids production. Non-OPEC production in 2030 is

projected to be 12 million barrels per day higher than in

2004, representing 35 percent of the increase in total

world production over the 2004 total. The estimates of

production increases are based on current proved

reserves and a country-by-country assessment of ultimately recoverable petroleum, as well as the potential

for unconventional liquids production.

The world oil prices in the IEO2007 reference case—and

in the high world oil price case—also are projected

to make previously uneconomical, unconventional

resources available. In 2004, world production of unconventional liquids totaled only 2.6 million barrels per day;

in 2030, in the reference case, unconventional liquids

production totals 10.5 million barrels per day (Figure 32)

and accounts for nearly 9 percent of total world liquids

production.

World Liquids Consumption

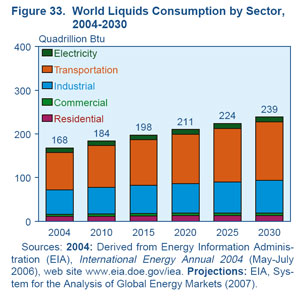

World liquids consumption in the IEO2007 reference

case increases to 118 million barrels per day (239 quadrillion Btu) in 2030, as the world continues to experience strong economic growth. Two-thirds of the increment in world liquids consumption in the reference

case is projected for use in the transportation sector,

where there are few competitive alternatives to petroleum (Figure 33). The industrial sector accounts for a

27-percent share of the projected increase, mostly for use in chemical and petrochemical processes.

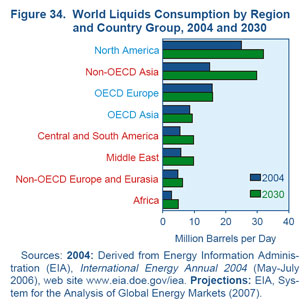

The largest increases in consumption between 2004 and

2030 are projected for North America and non-OECD

Asia, at 7 and 15 million barrels per day, respectively

(Figure 34). Outside North America, liquids consumption in the OECD regions generally grows more slowly,

reflecting expectations of slow growth or declines inpopulation and slow economic growth in most of the

OECD nations over the next two decades.

Strong expansion of liquids use is projected for the non

OECD countries, fueled by robust economic growth,

burgeoning industrial activity, and rapidly expanding

transportation use. The fastest growth in oil consumption is projected for the economies of non-OECD Asia,

averaging 2.7 percent per year from 2004 to 2030. For the other non-OECD regions, annual consumption growth

averages 1.0 percent in non-OECD Europe and Eurasia, 2.1 percent in the Middle East, 2.3 percent in Central and

South America, and 2.2 percent in Africa.

Non-OECD Asia accounts for 43 percent of the overall

increase in world liquids consumption, with projected

increases of 6.5 million barrels per day from 2004 to 2015

and another 8.5 million barrels per day from 2015 to

2030. China, India, and the other nations of non-OECD

Asia are expected to experience combined economic

growth of 5.8 percent per year from 2004 to 2030, the

highest rate among all the world regions. The robust

expansion of GDP projected for non-OECD Asia contributes to a 2.7-percent average annual increase in the

region’s liquids use.

World Oil Prices

The world oil price cases in this report are the same as

those in EIA’s Annual Energy Outlook 2007. In the reference case, world oil prices decline from $68 per barrel in 2006 to $49 per barrel in 2014, then rise to $59 per barrel in 2030 ($95 per barrel on a nominal basis). Total world

liquids consumption rises to 118 million barrels per day

in 2030 in the reference case. The low and high price

cases are included to illustrate uncertainties in the reference case projections (Figure 35). In the low price case,

world oil prices are projected to be $36 per barrel in 2030 ($58per barrel on a nominal basis). In the high price case, oil prices are projected to be $100 per barrel in 2030 ($157 per barrel on a nominal basis). The projections for total

liquids consumption in 2030 range from 103 million barrels per day in the high price case to 134 million barrels

per day in the low price case, indicating the substantial

range of uncertainty in the world’s future oil markets.

World Liquids Production

In the IEO2007 reference case, world liquids production

in 2030 exceeds the 2004 level by 35 million barrels per

day (Figure 36). Increases in production are expected for

both OPEC and non-OPEC producers; however, 65 percent of the total increase is expected to come from OPEC

areas. In 2030, OPEC is expected to produce 57 million

barrels per day and non-OPEC producers 61 million barrels per day in the reference case. Over the past two

decades, the growth in non-OPEC liquids production

has resulted in an OPEC market share substantially

below its high of 52 percent in 1973. In 2004, OPEC produced 41 percent of the world’s liquids supply. High oil

prices, new exploration and production technologies,

aggressive cost-reduction programs by industry, and

the emergence of unconventional resources contribute

to the outlook for continued growth in non-OPEC

liquids production.

The reference case outlook for liquids production was

formulated in a two-stage approach. The mid-term projections (through 2015) are based primarily on the current activities of the oil industry and national

governments, including: current production volumes;

recent rates of decline in output from producing fields;

planned exploration, development, and enhanced oil

recovery activities; country-specific policies and fiscal

regimes; and current conflicts and social unrest that

could interrupt production and make incremental

investments more risky. After 2015, the reference case

assumes that production decisions are made primarily

on economic grounds, based on assessments of the resource base, with less weight placed on current political conditions.

The IEO2007 reference case projects greater reliance on

OPEC oil supplies than was anticipated in last year’s

outlook. In IEO2006, OPEC’s total liquids production

(excluding Angola) was projected to increase by nearly

15 million barrels per day from 2003 to 2030; in IEO2007, the projected increase in OPEC production (excluding

Angola) is about 22 million barrels per day over the

same period. An extensive review of anticipated investment in exploration and production through 2015 was

conducted for IEO2007. As a result, the projections of

non-OPEC supply from several key producers were

lowered. However, the investment that several OPEC

members (notably, Saudi Arabia and Angola) currently

are making to expand their oil production capacity is

expected to more than offset the slower expansion of

non-OPEC supply projected in this year’s outlook.

There are several regions where production is restrained

through 2015 in the reference case. For instance, in the

key resource-rich countries of Mexico and Venezuela,

expected investment levels are lower than those

assumed in the IEO2006 reference case. In both countries, liquids production is projected not to expand (and,

in Mexico, to decline) until after 2015, when economic

decisions on investment allow production to improve.

Also, North Sea production is projected to decline more

rapidly than in last year’s outlook. The rate of decline in

North Sea production over recent years has been higher

than observed in earlier years, and economics do not

support a reversal of the declining trend in the IEO2007

reference case. In Iran and Iraq, political developments

are assumed to keep production levels fairly flat until

after 2015, when investment and production are projected to grow strongly through 2030.

IEO2007 includes supply estimates for the low and high

world oil price cases, based on the availability of world

crude oil resources. In the high price case, worldwide

crude oil resources are assumed to be 15 percent smaller

and therefore more expensive to produce than in the reference case, and the preferred production levels of

OPEC producers are reduced. In the low price case,

worldwide crude oil resources are assumed to be 15 percent larger and therefore less expensive therefore to produce than in the reference case, and the preferred

production levels of OPEC producers are increased. In

each of three oil price cases, a business-as-usual oil market environment is assumed. The IEO2007 cases do not

consider disruptions in oil production for any reason

(war, terrorist activity, weather, geopolitics).

Non-OPEC Production

The world oil prices projected in the IEO2007 reference

case allow non-OPEC suppliers to expand their production through 2030. Non-OPEC production increases

steadily in the projections, from 49 million barrels per

day in 2004 to 61 million barrels per day in 2030, as high prices attract investment in areas previously considered

uneconomical. The non-OPEC market share in 2030,

however, at 52 percent of the world’s liquids production, is lower than its 2004 share of 59 percent.

Non-OPEC conventional liquids production in the reference case increases from 47 million barrels per day in

2004 to 51 million barrels per day in 2015 and 53 million barrels per day in 2030, and unconventional liquids production from non-OPEC suppliers rises to 4 million barrels per day in 2015 and 8 million barrels per day in 2030. In the high world oil price case, non-OPEC unconventional liquids production rises to 11 million barrels per

day in 2030, as compared with 4 million barrels per day

in 2030 in the low price case, where most unconventional liquids are not economically competitive.

North Sea production is projected to decline more rapidly in the IEO2007 reference case than was projected in

IEO2006. Production from Norway, OECD Europe’s

largest producer, appears to have peaked at about 3.4

million barrels per day in 2001, and it is projected to continue declining to about 1.4 million barrels per day in

2030 as the larger and older fields mature. Production

from the United Kingdom, which peaked in 1999 at 3.0

million barrels per day, is projected to fall to 0.5 million

barrels per day in 2030.

Oil production in the non-OECD Europe and Eurasia

region is projected to reach nearly 15.0 million barrels

per day in 2015, based in large part on the potential

investment outlook for the Caspian Basin region, where

long-term production potential still is regarded with

considerable optimism. Caspian output more than doubles from the 2004 level to 4.3 million barrels per day in

2015 in the reference case and increases steadily thereafter. Current uncertainty about export routes from the

Caspian Basin region is assumed to be resolved.

North African producers Egypt and Tunisia produce

mainly from mature fields, and the IEO2007 reference

case assumes few additions to resources in the future. As a result, their production volumes decline gradually in

the projections. In East Africa, Sudan is expected to produce significant volumes by the end of this decade, with

the potential to exceed 700,000 barrels per day in 2010.

Eritrea, Somalia, and South Africa also have some

resource potential, but they are not expected to produce

significant volumes until late in the projections.

Several West African producers—Cameroon, Chad,

Congo (Brazzaville), Equatorial Guinea, Gabon, Mauritania, Niger, Sao Tome and Principe, and Ivory Coast—are expected to reap the benefits of substantial exploration activity, especially if current high oil prices persist.

West African producers with offshore tracts are expected to increase output by up to 1.1 million barrels

per day by the end of the projection period.

Oil producers in the Pacific Rim are expected to increase

their production volumes as a result of enhanced exploration and extraction technologies. India’s deepwater

prospects are expected to show some encouraging production increases in this decade, with the potential for

significant increases near the end of the projection

period. China’s conventional oil production is projected

to decline slightly, to about 3.3 million barrels per day in

2030.Vietnam’s long-term production potential is

viewed with considerable optimism, although exploration activity has been slower than originally anticipated.

Output from Vietnamese fields is projected to reach

504,000 barrels per day in 2015.

Malaysia is not expected to find significant new

reserves; its output has already peaked and is expected

to decline gradually through the end of the projection

period, to less than 500,000 barrels per day in 2030.

Papua New Guinea continues to add to its proved

reserves and is expected to achieve production volumes

approaching 110,000 barrels per day in 2015, followed

by only a modest decline over the remainder of the projection period. Exploration and test-well activity have

pointed to some production potential for Bangladesh

and Myanmar (formerly Burma), but significant output

is not expected until after 2010.

In North America, U.S. output that rises to 10.1 million

barrels per day in 2020 and remains fairly flat through

the end of the projection period is expected to be supplemented by significant production increases in Canada.

Canada’s conventional oil output contracts steadily in

the reference case, by about 0.5 million barrels per day

over the next 25 years, but an additional 2.5 million barrels per day of unconventional output from oil sands

projects more than offsets the decline in conventional

supplies. Since the publication of IEO2006, Mexico’s

state oil company, Petróleos Mexicanos (Pemex), has

announced annual production decline rates of 14 percent in its largest oil field at Cantarell [1]. The IEO2007

reference case does not anticipate adequate investments

through 2015, and as a result, production in Mexico is

projected to fall to 3.0 million barrels per day in 2015 (see

discussion on Reassessing the Potential for Oil Production in Mexico). IEO2007 assumes that declining revenue from oil production in Mexico ultimately will

encourage government action to increase investment

and technology access in the petroleum sector after 2015.

Given the country’s available resource base, such action

eventually should reverse the decline in production.

Liquids producers in South America have potential for

increasing output over the next decade. Brazil became a

million barrel per day producer of crude oil in 1999, with considerable production potential waiting to be tapped.

Brazil’s production rises throughout the projection period, to 3.9 million barrels per day of conventional

production and 0.5 million barrels per day of unconventional production in 2030. Colombia’s current economic

downturn and civil unrest have delayed development of

its oil production infrastructure, but its output is

expected to reach 700,000 barrels per day in 2015, with

continued modest increases over the remainder of the

projection period. Although the current political situation in Ecuador is in transition, there is still optimism

that Ecuador will increase production volumes over the

projection period.

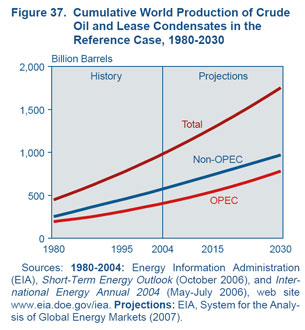

OPEC Production

It is generally acknowledged that OPEC members with

large reserves and relatively low costs for expanding

production capacity can accommodate sizable increases

in the world’s petroleum consumption. In the IEO2007

reference case, the production call on OPEC suppliers

grows at an annual rate of 2.0 percent through 2030

(Figure 37).

Amidst enormous uncertainty, Iraq’s role in OPEC in

the next several years will be of particular interest. In

1999, Iraq expanded its production capacity to 2.8 million barrels per day in order to reach the maximum

export revenue (slightly more than $5.2 billion) allowed

under United Nations Security Council resolutions.

Iraq’s oil production capacity in 2007 is assumed to be

2.0 million barrels per day [2]. Iraq has indicated a desire

to expand production aggressively, to more than 6

million barrels per day, once the security and political

situation in the country has stabilized. Preliminary discussions of exploration projects have already been held

with a number of potential outside investors. In the

IEO2007 reference case, Iraq’s oil production is projected

to reach 3.3 million barrels per day in 2015 and 5.3 million barrels per day in 2030.

Oil production in Iran is projected to increase only

slightly in the early years of the reference case, from 4.1

million barrels per day in 2004 to 4.3 million barrels per

day in 2015, despite the country’s sizable resource base.

In the long run, Iran’s oil production is projected to

reach 5.0 million barrels per day in 2030.

Kuwait and the United Arab Emirates (UAE) are

expected to follow similar growth paths in their oil production sectors. In 2004, levels of production from the

two countries were 2.5 and 2.8 million barrels per day,

respectively; in 2015, they are projected to be 3.2 and 3.8 million barrels per day, respectively; and in 2030 they are projected to be 4.1 and 4.9 million barrels per day,

respectively. Qatar’s production is projected to grow

from 1.0 million barrels per day in 2004 to 2.9 million

barrels per day in 2030, with liquids other than crude oil

expected to provide more than half the increase.

In the past, Saudi Arabia—with its very low development and production costs per barrel of output—has

maintained 1 to 5 million barrels per day of spare production capacity, which has given it considerable market power. It is expected to maintain average spare

capacity of 1 to 2 million barrels per day in the future. In the reference case, Saudi Arabia’s production is projected to be 9.4 million barrels per day in 2015 and 16.4

million barrels per day in 2030.

Angola became a 1.1 million barrel per day producer in

2004,and the results of deepwater exploration indicate

that its production could increase to as much as 4.0 million barrels per day by 2030. The rapid increase in

Angola’s production demonstrates the importance of

political stability, international investment, and technology advances. Angola’s oil production languished for

the most part during a 20-year civil war, which ended in

2003. It was not until the late 1990s, when prospects for a

peaceful resolution were taking shape, that the foreign

investment needed to support offshore production

began to materialize. Angola’s decision to join OPEC in

January 2007 is not expected to slow the increase in its oil

production, given that other OPEC members were

granted some flexibility while they were rapidly

expanding their production.

In the IEO2007 reference case, OPEC members outside

the Persian Gulf (excluding Angola) are projected to

increase their production capacity only moderately, in

part because of the relatively high cost of capacity

expansion in most of the member countries. There is

some optimism surrounding Nigeria’s potential for offshore production. For Algeria and Libya, the reference

case projects an increase of 1.2 million barrels per day in

their combined liquids production from 2004 to 2015,

but after 2015 it is projected to remain fairly flat. Indonesia’s production is expected to decline over the projection period, and Venezuela is expected to see some

increase in production after 2015.Tables G1-G9 in

Appendix G show the ranges of production potential for

both OPEC and non-OPEC producers.

Geopolitical issues in a number of the OPEC countries,

including Iraq, Iran, Venezuela, and Nigeria, make it difficult to estimate future production levels. As a result,

there is a high level of uncertainty associated with the

reference case assumptions and projections for OPEC

production through 2030.

The IEO2007 high price case provides one scenario in

which OPEC limits production. Assuming lower availability of non-OPEC conventional resources, OPEC

would be able to exercise greater influence on oil prices.

Production of both OPEC and non-OPEC conventional

liquids is projected to increase in the high price case, but

at a slower rate than projected in the reference case.

Because higher prices would make more unconventional liquids production economically competitive,

non-OPEC liquids production is projected to be nearly

the same in the reference and high price cases, with

unconventional liquids replacing most of the reduction

in conventional production that is projected in the high

world oil price case.

The IEO2007 low price case assumes greater availability

of non-OPEC conventional resources than in the reference case. Oil prices fall as non-OPEC production

expands, and OPEC producers must increase production to meet their revenue requirements. As a result,

OPEC’s options for influencing the market are limited.

In the low price case, OPEC production is projected to be

about the same as in the reference case, but with lower

total revenues.

Oil Reserves and Resources

Historically, estimates of world oil reserves have generally trended upward (Figure 38) [3]. As of January 1,

2007,proved world oil reserves, as reported by Oil & Gas Journal,7 were estimated at 1,317 billion barrels—24 billion barrels (about 2 percent) higher than the estimate for 2006 [4] (Table 3). In addition to growth in remaining

oil reserves, production from conventional crude oil and

condensate reserves, natural gas plant liquids, Canadian

oil sands, and Venezuelan ultra-heavy oil during 2006

were estimated to be 30 billion barrels. Taken together,

the reserve increases and production imply that 54 billion barrels of reserve discoveries and growth occurred

during 2006, or an increase of about 4 percent.

Reserve estimates for oil, natural gas, and coal are difficult to develop. EIA develops estimates of reserves for

the United States but not for foreign countries. As a convenience to the public, EIA makes available global

reserve estimates from the Oil & Gas Journal, World Oil,

and BP’s Statistical Review of World Energy, and uses the

data in its analyses.

Proved reserves of crude oil are the estimated quantities

that geological and engineering data demonstrate with

reasonable certainty can be recovered in future years

from known reservoirs, assuming existing economic

and operating conditions. Companies whose stocks are

publicly traded on U.S. stock markets are required by the Securities and Exchange Commission (SEC) to report

their holdings of domestic and international proved

reserves, following specific guidelines. Country-level

estimates of proved reserves are developed from the

data reported to the SEC, from foreign government

reports, and from international geologic assessments.

Estimates are not always updated annually, and some

countries invest in exploration only to maintain a target

level of proved reserves. Thus, historical data series may

be relatively flat over some periods, with sudden jumps

in others.

Since 2000, the largest net increase in estimated proved

oil reserves has been made in Canada, with the addition

of 174 billion barrels of Canadian oil sands as a conventional reserve.8 Iranian oil reserves have increased by

46.6 billion barrels, or 52 percent, since 2000. Kazakhstan has had the third-largest increase, 24.6 billion barrels,

since 2000. The 10 countries with the largest net

increases in reserves between 2000 and 2007 are listed in Table 4. According to Oil & Gas Journal, 56 percent of the world’s total proved oil reserves are located in the Middle East (Figure 39). Among the top 20 reserve holders in 2007,11 are OPEC member countries that, together,

account for 65 percent of the world’s total reserves (Table 3). The largest declines in oil reserves between

2000 and 2007 were reported in Mexico (16.0 billion barrels), China (8.0 billion barrels), Norway (2.9 billion barrels), Australia (1.3 billion barrels), and the United

Kingdom (1.3 billion barrels).

The most common measure of the adequacy of proved

reserves relative to annual production is the reserve-to

production (r/p) ratio, which describes the number of

years of remaining production from current proved

reserves at current production rates. For the past 25

years, the U.S. r/p ratio has been between 9 and 12 years, and the top 40 countries in conventional crude oil production rarely have reported r/p ratios below 8 years.

The major oil-producing countries of OPEC have maintained r/p ratios of 20 to 100 years (Table 5).

Notes and Sources

References

Chapter 3 Tables

|